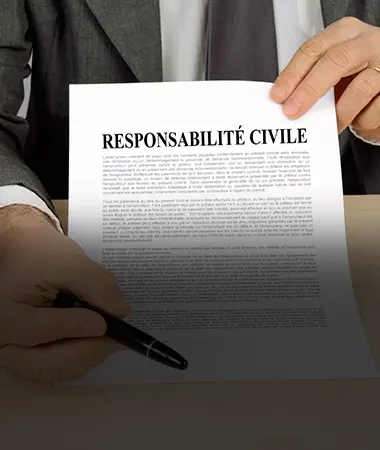

Responsabilité civile pro

Cette assurance couvre les dommages causés à autrui dans le cadre de l’activité professionnelle. Elle protège ainsi l’entreprise contre les réclamations.

Pertes financières

Cette garantie prévoit le remboursement des pertes financières dues à un préjudice, telles que les pertes de chiffre d’affaires ou les frais de remise en état.

Locaux et risques auto

Ce type de contrat assure les installations et les véhicules professionnels contre les dommages, le vol ou l’incendie par le biais d’une compensation..